Resilience through Reform

BUDGET SNAPSHOT

The government is proposing a tax reform package with 3 parts:

a “fairer” tax system for workers, first home buyers and future generations

a “better” tax system for businesses by encouraging investment and innovation, and

a “simpler and more sustainable” tax system.

Details of the highly anticipated initiatives to improve housing affordability have emerged. While negative gearing for residential property will be limited to new builds from 2027–28, all existing investments made before 7:30pm AEST on 12 May 2026 will be grandfathered. As for capital gains tax (CGT), the 50% discount will be replaced with cost base indexation from 1 July 2027, with a minimum 30% tax rate on realised gains.

This will apply to all CGT assets, including pre-CGT assets, except new builds. It will be prospective, with gains accrued on existing investments prior to 1 July 2027 to retain the 50% discount.

Other notable measures include those relating to discretionary trusts, a new tax offset for working Australians and the gradual reduction of the Fringe Benefits Tax (FBT) discount for affordable electric vehicles.

In particular, discretionary trusts will be taxed at 30% from 1 July 2028. With trusts historically not being taxed as separate entities, this measure will have significant implications for individuals and businesses alike. To ease the cost-of-living pressures, an annual working Australian tax offset of $250 is proposed for eligible Australian workers. The current FBT discount for affordable electric vehicles will transition to a permanent 25% discount progressively over 3 phases.

The Budget measures are additional to recent developments, including:

the temporary reduction of excise and excise-equivalent customs duty rates for most fuel products from 1 April 2026 to 30 June 2026

the release of exposure draft legislation for the instant $1,000 tax deduction for work-related expenses

the release of exposure draft legislation for strengthening the foreign CGT regime in Div 855 of ITAA 1997, including the transitional CGT discount for certain renewable energy assets, and

the release of a consultation paper on options to strengthen the annual superannuation performance test.

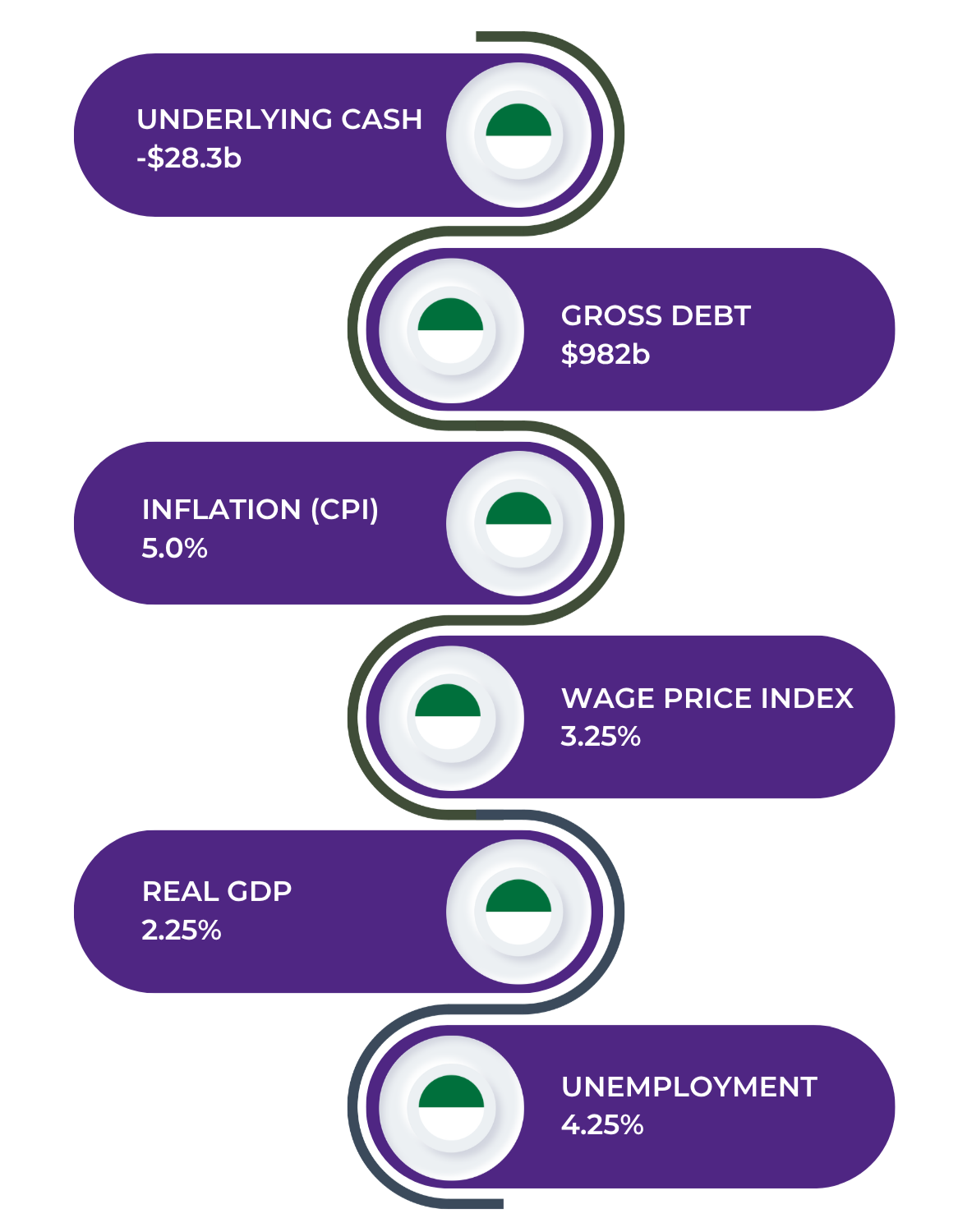

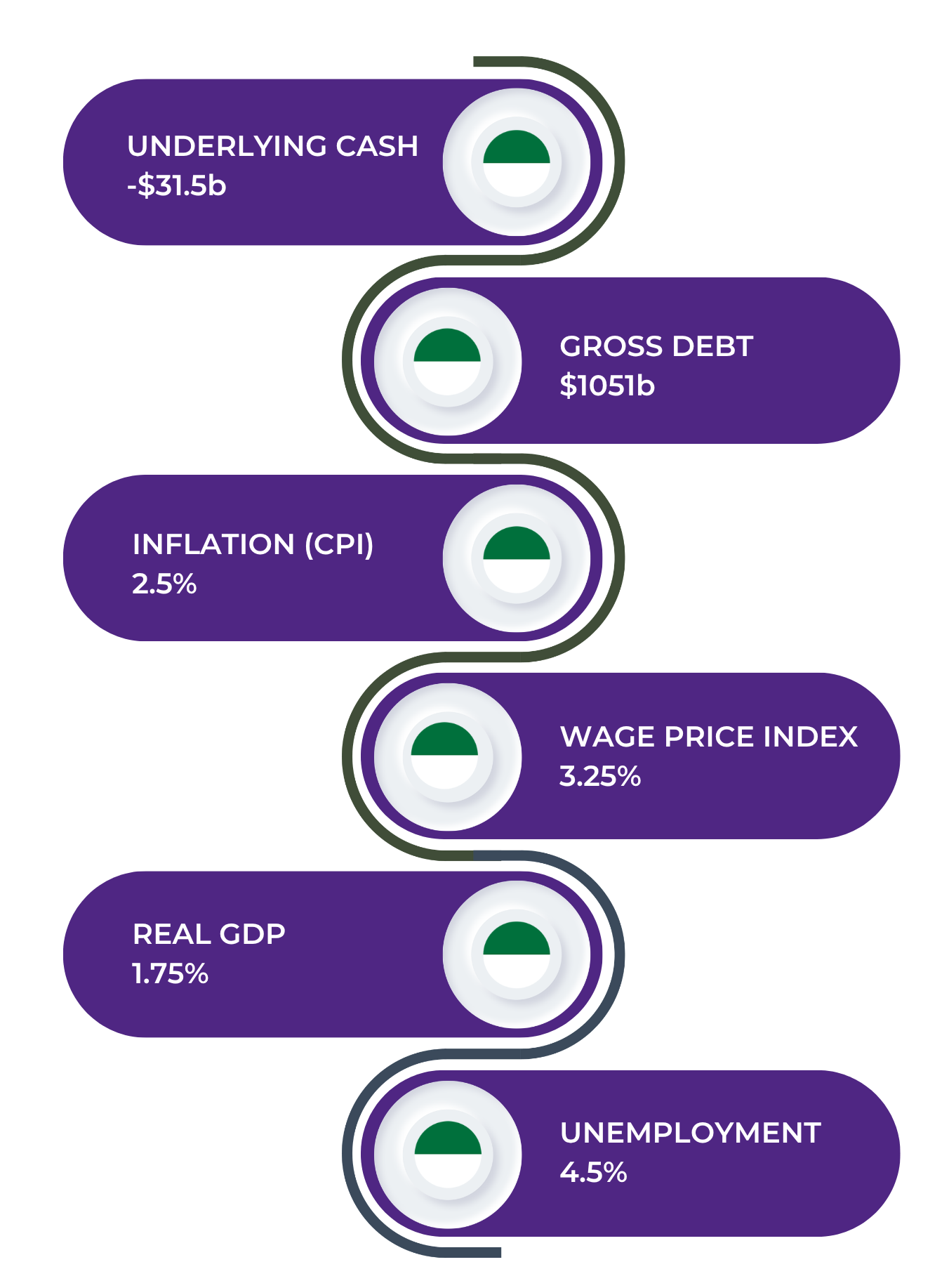

ECONOMIC OUTLOOK AND FORECASTS

2025-26

2026-27

KEY AREAS

COST OF LIVING RELIEF

HOUSING + INFRASTRUCTURE

TAX REFORM

FUEL SUPPLY + RESILIENCE

BUSINESS PRODUCTIVITY

2026-27 HIGHLIGHTS

-

The 50% CGT discount will be replaced with cost base indexation for all CGT assets (except new homes) from 1 July 2027, with a 30% minimum tax on realised gains also applying from that date.

A minimum tax rate of 30% will be payable by trustees of discretionary trusts from 1 July 2028.

-

Negative gearing for residential property will be limited to new builds from 1 July 2027, with no change for existing arrangements.

Each working Australian taxpayer will receive a $250 Working Australians Tax Offset from the 2027–28 income tax year.

The Medicare levy low‑income thresholds for singles, families, and seniors and pensioners will be increased by 2.9% from 1 July 2025.

The temporary restrictions on foreign ownership of housing will be extended, and Australia’s foreign investment framework will be strengthened.

The age-based uplift of private health insurance rebate (the PHI rebate) will be removed from 1 April 2027.

Payment of the full rate of pension supplement will be extended from 6 weeks to 12 weeks for recipients who are temporarily absent from Australia.

The pension supplement will cease for those who are residing permanently overseas or who are temporarily absent for more than 12 weeks.

-

Australia will transition to a permanent 25% discount on FBT for certain electric vehicles.

The instant asset write-off of $20,000 for small businesses applying the simplified depreciation rules has been extended permanently.

Companies with up to $1 billion in turnover will be eligible to carry back tax losses for up to 2 years from 1 July 2026.

Small start-ups in their first 2 years of operation will be able to get a refund for tax losses capped to the value of tax remittances relating to employment from 1 July 2028.

Reforms have been announced to the R&D tax incentive from 1 July 2028 as part of the government’s response to the Ambitious Australia: Strategic Examination of Research and Development Final Report.

The venture capital limited partnership (VCLP) and early stage venture capital limited partnership (ESVCLP) tax incentives will be expanded from 1 July 2027. The eligible venture capital investor program will be closed to new applications from 12 May 2026 7:30pm (AEST).

The global and domestic minimum tax legislation will be amended from 1 January 2026 to implement the side-by-side package agreed by the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting on 5 January 2026.

-

Deductible gift recipients list to be updated.

-

Access to refunds of indirect tax under the Indirect Tax Concession Scheme has been extended.

More nuisance tariffs will be abolished from 1 July 2026.

The duty exemption for goods imported from Ukraine will be extended for a further 2 years to 3 July 2028.

Funding will be provided, and measures will be introduced to combat the illicit tobacco market.

-

Access to monthly reporting and payments as well as dynamic PAYG instalment calculations will be expanded for small and medium businesses from 1 July 2027.

Funding will be provided, and measures will be introduced, to protect and strengthen the tax system against fraud.

Funding will be provided from 2026–27 to strengthen governance requirements, supervision and enforcement in relation to managed investment schemes.

Funding will be provided to the ATO and other government organisations from 2026–27 to meet the government’s commitments under the Digital ID Act 2024 and maintain the security and reliability of the government’s Digital ID System.

Funding will be provided over 2 years from 2026–27 to streamline regulatory systems and secure access to data, including the synchronisation of director information, uplifting ABN authentication and completing the transition of ABN and superannuation lookup functions to the ATO. Legislation will also be introduced to improve regulation in the financial sector.

Funding will be provided from 2026–27 to address systems abuse in the child support scheme. This includes improving the accuracy of child support assessments by strengthening tax lodgment enforcement, extending Single Touch Payroll data sharing and expanding the use of employer withholding to ensure more child support is paid in full and on time.

Reforms to harmonise state payroll tax administration frameworks will be explored as part of the government’s national competition policy (NCP).

-

The Budget announces a new Tax Offset deduction for income earners to take effect from the 2027-28 income year. (Paid in 2028-29.) The Working Australians Tax Offset (WATO) provides an additional tax cut of up to $250 for most income earners.

-

Under the changes to negative gearing announced in the Budget the Government will limit new negative gearing claims to new housing builds from 1 July 2027. But the Budget Papers say, “Existing arrangements will remain unchanged for all properties held before Budget night, and investors who buy new builds will still be able to deduct losses from other income.

-

The Budget reintroduces loss carry back for small business and loss refundability for start-ups. From 2026–27, eligible companies who make a loss will be able to use that loss to get a refund against tax paid in the prior two income years. The Government is also introducing loss refundability to support new start-up businesses.

-

As widely forecast before the Budget the Government is replacing the existing 50 per cent Capital Gains Tax discount with an inflation-adjusted system. However the change goes much further than was widely forecast, applying to existing assets, but with the new arrangements only applied to gains from 1 July 2027. Under the new system, real gains will be taxed at a minimum rate of 30 per cent. Investors in new housing will be able to choose the existing 50 per cent CGT discount or the new arrangements.

-

The Budget announced the Government will introduce a minimum tax of 30 per cent on discretionary trusts from 1 July 2028. The change is forecast to reduce the tax take in the first three years but then jump to $4.4 billion in 2029-30, the second largest improvement in the Budget over the Forward Estimates after changes to the NDIS.

-

The Budget permanently extends the $20,000 instant asset write-off (IAWO) for small businesses from 1 July 2026, for small businesses with turnover up to $10 million.

-

The Budget announces a new Tax Offset deduction for income earners to take effect from the 2027-28 income year. (Paid in 2028-29.) The Working Australians Tax Offset (WATO) provides an additional tax cut of up to $250 for most income earners.

-

Ahead of the Budget the Albanese Government announced a major overhaul of the National Disability Insurance Scheme designed to save $35 billion in expected cost increases over the next four years and a claimed $150 billion over the next decade.

-

As part of a major shakeup in the health, disability and aged care portfolios, the Government announced ahead of the Budget that it will abolish the controversial aged care co-payment for people receiving in-home assistance with showering, dressing and support in managing continence. The change will be funded by the abolition of the additional private health insurance rebate paid to those over 65 with private insurance.